(By Trygve Christiansen and Eli Wærum Rognerud, OAG Norway)

(See full paper on the shale gas revolution, including policy, geopolitical and environmental effects here: link)

Shale gas has been described as a “revolution”, our “bridge to a low carbon future” and indeed “the biggest thing that happened to America”, yet others have branded it an “environmental disaster”. There is little dispute however that the commercial exploitation of shale gas has been, and continues to be, a major game changer in the global energy sector. This article briefly explains the nature of the shale gas boom, its effect on gas markets and prices, and the potential impact on current and aspiring gas and oil producers in developing nations.

What is shale gas?

Shale gas, along with tight sands and coal bed methane constitutes so-called unconventional gas resources. These are natural gas resources trapped in deep, underground rocks such as shale rock or coal beds (Carbonbrief 2015). The resources are harder and more expensive to access than for example conventional gas, but can be extracted using hydraulic fracturing, or “fracking”; a method whereby a mixture of water, sand and chemicals are injected into the rock formation under high pressure, fracturing the low-permeability shale to release natural gas. The method has been used in the industry since the nineteenth century and in the US since the mid twentieth century, but has recently become much easier and much cheaper as a result of improved techniques and technologies. (Marey and Koopman 2013, 2; Carbonbrief 2015)

Shale rock is common in many parts of the world, and makes up an estimated 35% of the world’s surface rocks. Technically recoverable shale gas resources exist in a number of countries, however it is the USA that has piloted the “revolution” and today by far dominates the industry. US shale gas production in 2012 stood at some 460 billion cubic meters (bcm) gas, followed by Canada (80 bcm), Poland (0,66 bcm) and China (13,4 bcm) (IEA 2015b).

The nature of the boom

The development has been rapid. Between 2007 and 2014, US shale gas production grew more than 50 percent, with a five-fold increase in proven national reserves in the same period. Though not the main focus of this article, it should also be noted that oil production from shale deposits, so-called “tight oil” is growing even faster than shale gas, bringing US oil production to a level not experienced since 1970. Of total marketed gas production in the US, 60% are now unconventional gas resources. (IEA 2014; Statoil 2015). Though there is considerable uncertainty still surrounding production forecasts, the IAE estimates that global natural gas reserves, including shale gas, will last 250 years with current consumption levels, compared with 120 years when only including conventional recoverable resources (IEA 2011, 7).

When launching the IEA Energy Outlook Report in 2012, Executive Director Maria van der Hoeven left little doubt about the significance of the shale gas revolution: “North America is at the forefront of a sweeping transformation in oil and gas production that will affect all regions of the world”, she stated to the press (IEA 2013a). The key to this transformation is first and foremost the sheer volume of gas production, but also the -at least longer term – possible flexibility with which US gas can be traded.

Natural gas made up 21% of the world’s energy supply in 2011 (IEA 2014), and demand is rising. According to the IEA, gas is especially attractive to developing regions in Asia, most notably China and India, and the Middle East, which face rapid urbanization and growing energy demand. In its special report on gas in 2011, “The golden age of gas?” IEA outlines a scenario where the share of natural gas in the global energy mix rises to 25% by 2035. This assumes a gas demand of 5,1 trillion cubic meters (tcm), 1,8 tcm more than current levels.

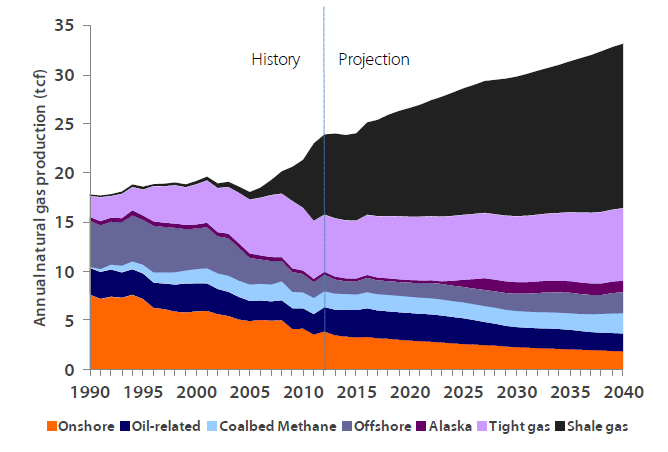

Unconventional natural gas resources are now estimated to be as large as conventional ones (IEA 2011), and the portion of shale gas of total production is expected to grow significantly, as illustrated in figure one.

Effect on prices and markets

So far, the most important effects of the shale gas boom are observed in the US, where a positive supply shock has fuelled demand and at the same time a significant downward pressure on natural gas prices 2010-2014 (Fatouh, Rogers and Stewart, 2015, 24; IEA 2015, EAI 2015a).

US gas prices are quoted by the Henry Hub index, reflecting the pricing point of natural gas futures contracts traded on the NY Mercantile Exchange, NYMEX. Spot prices are given in USD/MMBtu, or million British thermal units. From peaks well above 10USD/MMBtu in 2006-08, prices on the Henry Hub for a period dropped below USD2/MMbtu but have now stabilized between USD3 and USD4/Mmbtu. In terms of market position, this development has moved the US from a major gas importer to a position of energy self-sufficiency and potential net export within few years (IEA, 2012a).

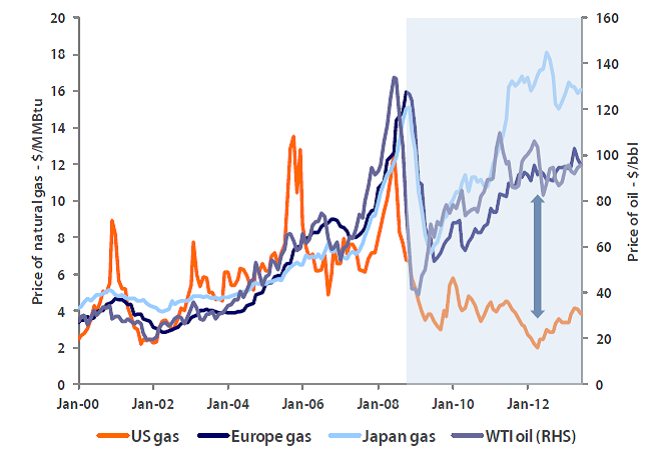

The US supply boom has further broken the historically stable relationship between the price of oil and Henry Hub Natural gas. Most importantly, it has increased the price differential or spread of gas prices between the US on the one hand and Europe and Asia and Japan on the other, resulting in geographically divided, three-tier gas pricing structure. This means Henry Hub is selling at a fourth of European prices and a fifth of Japanese, as illustrated in Figure 4 (Maroy and Koopman 2013, 2).

These developments have in turn affected the global trading pattern of gas, and to some extent the energy mix in different regions.

As indicated above, virtually all US gas is currently traded in the domestic market as there are no natural gas export facilities in operation yet, though several are underway. Overseas export is expensive, requiring either a gas pipeline or LNG production facilities. As a result, LNG imports that had been expected to reach 70 Bcm in 2010, were in fact reduced from 18 Bcm in 2005 to 4,2 Bcm in 2012. This has meant that volumes from other gas producers originally intended for the US market has had to find new buyers. Qatar, as the world’s largest LNG exporter, whose record-size LNG compressors (megatrains) launched in 2009 expanded capacity in a low-demand period, were able to divert volumes to both Europe and Asia. Declining demand in Europe and readily available Qatari LNG led to a drop in pipeline imports in Europe, mainly from Russia. Russia in the period proved itself as a “shock absorber” of an increasingly integrated market, reducing its pipeline exports (Fattouh, Rogers and Stewart 2015, 22). Asian demand had suffered from the financial crisis of 2008, but rapidly recovered and soared in the 2010-11, partly due to the Fukushima disaster, after which Japan used gas to replace its nuclear power (BP, 2014; OPEC 2014a). The Asian demand was then in part met by the Gulf surplus created in the wake of increasing US self-sufficiency.

Notwithstanding these important supply shifts, the perhaps most important impact is possibly still to be seen, when the US position itself as an exporter. Whilst the US prohibits exports of crude oil and condensate, there are much fewer restrictions on natural gas. Export is already approved to countries with which US has a free trade agreement (Irwin 2013), and in May this year, US president Obama gave green light for another milestone LGN export project. Cheniere Energy’s proposed liquefaction terminal in Corpus Christie bay, Texas, became the sixth LNG to win approval for global gas export. Over the next 20 years, Cheniere will be allowed to export up to 2.1 billion cubic feet of LNG per day to countries with which the United States does not have free trade agreements (Dlouhy, 2015). With more than half a dozen such terminals planned, Cheniere is positioned to become one of the world’s most important gas exporters in the global energy market. Many more investors have sought approval for similar export projects as federal policy on the issue is expected to relax further. License to export unrestrictive of destination and a strategic geographic position means that not only export volume, but flexibility, may pave the way for the US as the new global “swing supplier” in gas. However, uncertainty surrounding the technical as well as financial viability of many of these projects, political resistance and industry lobby fighting to keep the “cheap gas at home” leaves forecasts uncertain (Blackwill and O’Sullivan 2014).

Since oil, gas and coal are to some extent substitutes, shale supply also has had an impact on the market of other energy sources. In the US, low gas prices has made it competitive to coal and helped reduce consumption, though the US also has the world’s largest reserves of coal. US Coal output dropped from some 160 million MWh in 2002 to nearly 120 million MWh in 2012. Coal exports soared in the same period, from a quarterly figure of just over 20 million MWh on 2002, to a peak over 160 million MWh in 2012 (IAE, 2013). The US shift from coal to gas is further helped by government policy to reduce coal, and increasing shares of renewable source in electricity generation (OPEC 2014b). Consequently, according to OPEC (2014a, 8) “US coal has found its way into European markets, where its relative low price coupled with low carbon prices has made it more competitive in power generation than gas.” In fact, 50% of US coal exports was absorbed by Europe in 2012 (Maroy and Koopman 2013, 3). Also in Asia, coal is still far cheaper than natural gas, and demand outlook depends as much on Co2 prices and government policies as the volume of shale gas on the global market. Analysts at Rabobank also found a strong negative price relationship between oil and gas prices when relative supply of gas over oil increased 2000-2013 (IEA 2014; Maroy and Koopman 2013).

Developing country effects

The recent drop in oil and gas prices, largely tributed to the shale oil and gas boom, has a negative effect on oil and gas companies’ willingness to invest in developing countries, especially in Africa. PwC[1] carries out an annual survey among these companies asking them to rank factors that are likely to impact their oil and gas business in Africa. In 2014 the oil and gas prices were ranked as fourth, but in 2015 in jumped to number one. The price is regarded as more important than “protectionist governments” and “inadequacy of basic infrastructure”. This means that African countries with oil and gas reserves are feeling the effects of an external price factor which they cannot influence. This coincides with a drop in Africa’s share in world’s total oil production, going down from 10,1 % in 2013 to 9,6 % in 2014. Given that Africa is seen as an upcoming oil and gas region, this trend is not positive.

Several countries in Africa are affected by the shale oil and gas revolution. The drop in oil prices has contributed to delays in investments in some countries. In Uganda several workers in the oil industry has been laid off this year and in Tanzania the decision on whether to develop the discovered gas fields and build a much needed LNG plant is regularly delayed. Kenya[2]has been seen as a country with great potential for extraction of petroleum resources, but the exploration activities has slowed down lately. Recent studies conclude that for projects in Kenya to make profit, oil price needs to be at a minimum of 70 USD per barrel. Currently, the oil price sits at approximately 50 USD per barrel. In Ghana, the 2015 government budget was based on an estimated oil price of 99,38 USD. With the sharp drop in oil price, the government experienced a big budget deficit. This deficit was covered by withdrawing funds from the Ghana Stabilization Fund, which contains petroleum revenue[3].

While the drop in oil and gas prices may be hurting the industry and potential revenue, it may be good news for those buying refined products such as petrol and kerosene. It may also be good news for countries that spend a lot of money on subsidizing such refined products for its citizens, such as Nigeria and Venezuela. The problem however is that countries that apply big fuel subsidies also rely heavily on petroleum revenue.

The development in the shale industry and potential effects on global oil and gas prices will be closely watched by developing country leaders, investors and companies alike.

References

Blackwill, Robert and O’Sullivan, Meghan. 2014. “America’s Energy Edge: The Geopolitical Consequences of the Shale Revolution” In The International Relations and Security Network. 18 March. Accessed 13 July 2015. http://www.isn.ethz.ch/Digital-Library/Articles/Detail/?id=177844

Fattouh, Bassam, Rogers, Howard V. and Stewart, Peter. 2015. The US shale gas revolution and its impact on Qatar’s position in gas markets. Columbia: Center on Global Energy Policy

IEA. 2013a. World Energy Outlook. Paris: IEA

IEA. 2014. Key World Energy Statistics. Paris: IEA

Marey, Philip and Koopman, Stefan. 2013. The macro-economic effect of the shale gas revolution. Utrecht: Rabobank International http://www.raobanktransact.com

OPEC. 2014a. World Oil Outlook. Vienna: OPEC

OPEC. 2014b. Joint IEA-IEF-OPEC Report on the Second Symposium on Gas and Coal Market Outlooks. Paris 30 October 2014. Accessed on 1 Aug 2015. http://www.opec.org/opec_web/static_files_project/media/downloads/publications/Joint_Summary_Report_of_the_2nd_Gas_and_Coal_Symposium_Oct2014.pdf

Statoil. 2015. The future of shale gas (Norwegian page). Accessed 1 August 2015. http://www.statoil.com/no/OurOperations/ExplorationProd/ShaleGas/Pages/TheImportanceOfShaleForStatoil.aspx