Cooperative audits have been carried out in INTOSAI with different objectives and methodologies. In most cases, they are tools to study and analyze policies of regional and international interest. More recently, the cooperative audits have also been used as part of a strategy for capacity development. Under the Organisation of Latin America and Caribbean Supreme Audit Institutions (Olacefs), the SAIs of Brazil, Colombia and Peru jointly investigated oversight of public revenues from the oil and natural gas exploration and production.

By the Federal Court of Accounts (Tribunal de Contas da União) Brazil, Chair OLACEFS

This coordinated audit is part of a cooperation project between Olacefs and GIZ, and was carried out mainly in 2013, with a final report published in 2014. The topic of the oversight of public revenues from the oil and natural gas exploration and production was defined as a priority by the Olacefs Regional Training Committee (CCC). The hydrocarbon production is a relevant economic activity for many Latin American countries because, besides its strategic energy importance, it generates significant impacts on public revenues, mainly by collecting government takes. As a result, the appropriate oversight of these resources, by the State, is a sensible issue, mainly considering the involved amounts – only in Brazil almost US$ 13 billion were collected in 2013.

Methodology

The institutional model set for the hydrocarbon exploration and production, as well as how the oversight of these activities is performed, differs a lot among countries. The Federal Court of Accounts (TCU), with the consulting assistance provided by EnerRio, carried out a study on the institutional conditions related to the control of public revenues from oil and natural gas exploration and production activities in some of Olacefs countries. The study was funded by GIZ and included the following countries: Argentina, Bolivia, Brazil, Colombia, Ecuador, Mexico, Peru, and Venezuela.

Based on this institutional analysis, it was possible, therefore, to identify common challenges and potential topics of interest for the conduction of coordinated audits among these SAIs.

Thus, the topic selected for this audit was related to the integrity, reliability and transparency of the processes in oil and natural gas production measurement and in the calculation and payment of government takes as a result of this Production.

The selection was done considering that this topic is a starting and comprehensive point, capable of providing a wide analysis based on which new questions, sometimes specific for each country, become visible.

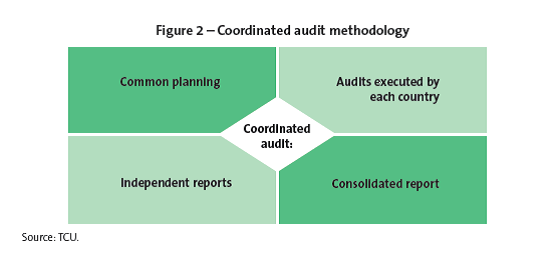

Each participating SAI carried out an audit in its own country, based on common guidelines. The TCU was responsible for the general planning, coordination of tasks and consolidation of the final obtained results.

Purpose and scope

The purpose of this coordinated audit is to evaluate the regulatory, institutional and operational conditions of the governmental agencies and entities in charge of the control of the oil and natural gas production measurement and of the calculation and payment of the government takes, identifying eventual bottlenecks and opportunities for improvement, as well as good practices for management optimization.

Based on this general purpose, three analysis focus were defined: (1) to what extent the control of oil and natural gas production measurement performed by the regulatory entity has the required principles to reasonably ensure reliability and integrity of the produced volumes; (2) to what extent the control of the calculation and payment of the government takes from oil and natural gas exploration and production performed by the regulatory entity has the required principles to reasonably ensure reliability, integrity and timing of the values; and (3) to what extent the data and the information related to the oil and natural gas production measurement and the calculation and payment of the due government takes are officially made available, in a transparent, accessible and friendly manner, in order to allow for its replicability by a third party, outside the process.

Findings and conclusions of the audit itself vary between the countries, and will be presented at the 2nd WGEI meeting in Oslo in September 2015. In general however, participating SAIs concluded that the process of collaborative audit was highly successful.

First of all, its conduction enabled the approach of relevant topics in the national environments and with similarities and common interest topics with other countries, which allowed for the creation of a wider and more complete vision regarding the faced problems and the different solutions applied in each situation.

In addition, although the audits individually developed by each SAI have been carried out in accordance with each country characteristics, the success of this coordinated audit showed that it is possible to analyze the issue based on common interest points and under perspectives not restricted to the SAIs themselves, which, subsequently, enables external control entities to extrapolate their traditional line of thought and try new points of view. In this sense, it is highlighted the knowledge acquired by the teams involved in the work regarding oil and natural gas production measurement and government takes processes, including technical visits made, whether individually or in Group.

To learn more about the use of collaborative audits in the OLACEFS, check out this latest INTOSAI IDI newsletter article: http://intosaidevelopmentinitiative.cmail2.com/t/ViewEmail/t/3CAEC77D3F5F97B1/850AC1FC67AFF6D9F6A1C87C670A6B9F